The Infinite Banking Concept is a strategy that relies on dividend-paying, whole life insurance to store money while waiting for investment opportunities.

The purpose: to grow wealth and become better, more patient investors.

And although the concept has been around for decades, there is still much misinformation and confusion regarding the subject.

In this article, we explore the pros and cons of Infinite Banking to better understand where it is worthwhile and where it falls short.

Pro: Money Out of Wall-Street

The first pro of Infinite Banking is getting money out of Wall Street and needless, high-risk investments.

The goal of Wall Street is to do one thing–get more money under management.

But most individual investors do not benefit from the Wall Street methodology.

For starters, individual investors typically underperform the market. One study showed that over the last 20 years, individual investors earned an average of 4.25% per year compared to the S&P 500’s 6.06%.

On top of this, not one mutual fund has consistently beaten the market over the last five years.

All this, combined with the significant risk of stock market crashes, is the reason many individuals want out.

Most of those involved with the Infinite Banking Concept do so because they seek competitive ways to invest money outside of Wall Street.

This is the first pro of Infinite Banking.

Con: Takes Time to Build Value

On the downside, Infinite Banking takes time.

The longer timeframe is because Infinite Banking uses whole life insurance, which has restrictions.

You put money in a bank account, bond, CD, or almost any other investment, and that money is immediately available.

But, whole life insurance doesn’t work this way.

Regulations around whole life insurance say there can only be a certain percentage of capital, or cash value, as a percentage of the total life insurance coverage during the first years of the policy.

Here is the typical schedule for building cash value.

- Year 1: 50-65% of premiums available.

- Year 5: 85-95% of premiums available.

- Year 10: 105-110% of premiums available.

- Year 15: 120-130% of premiums available.

- Year 15+: Continuous dividend growth.

Infinite Banking policies take time to build, making Infinite Banking more complicated compared to other investments.

Pro: High Potential Growth Rate

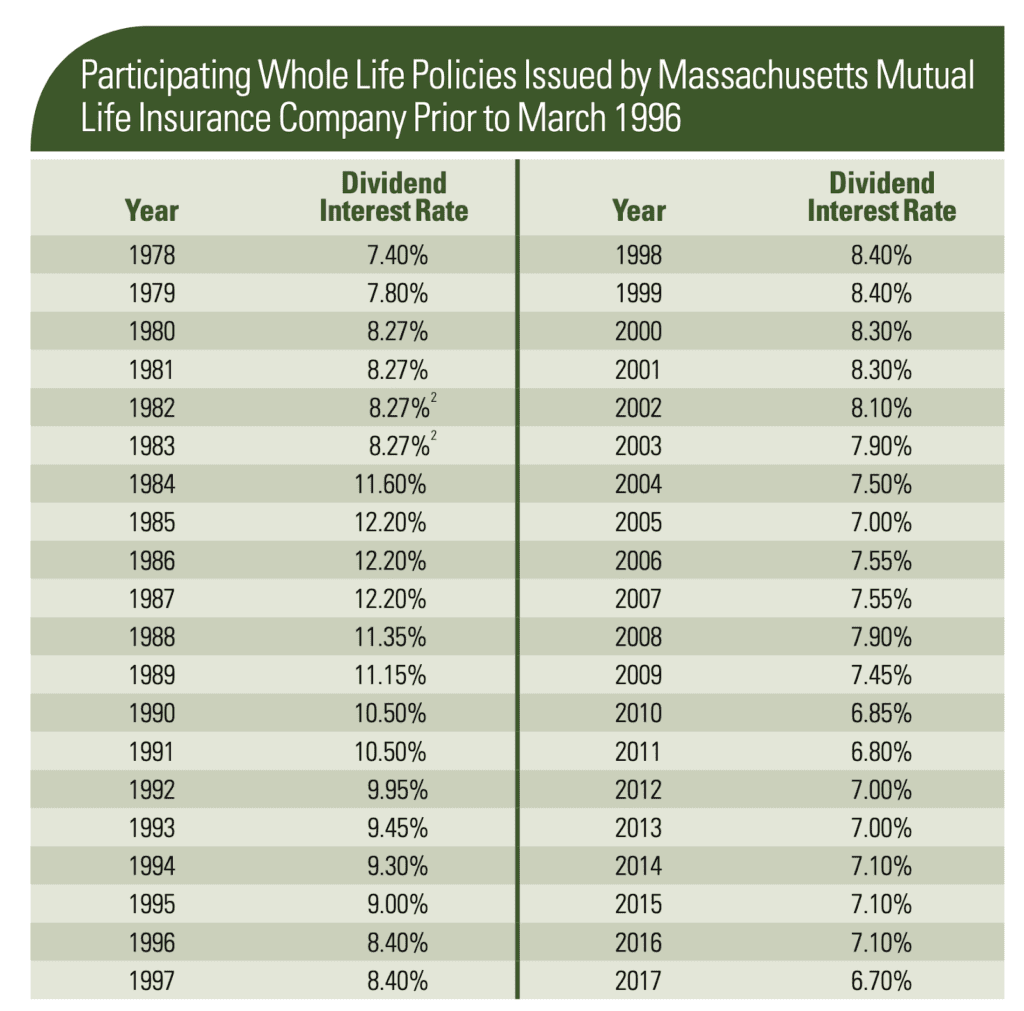

The next pro of Infinite Banking is the high potential growth rate compared to other savings-type investment vehicles.

One study (above) showed that a whole life insurance policy grew at an average of 8.61% over 30 years (1978-2017).

Compared to bonds, CDs, money market, or bank savings accounts, whole life insurance often performs significantly better.

There is no other savings vehicle better for high growth while still having access to capital for investments, than Infinite Banking and whole life insurance.

High potential growth makes whole life insurance an attractive place to save money.

Con: Cost of Insurance

The next downside is the cost of insurance.

Whole life insurance is regulated. As such, an individual must have a certain percentage of their premium paid towards life insurance in the first years of the policy.

The cost of insurance makes Infinite Banking more expensive in the first years.

And if the policy is canceled in the first couple of years, you won’t get that capital back.

Insurance costs can also vary based on the individual, age, health, and other factors that can make an Infinite Banking policy look better or worse.

The insurance cost is a potential barrier to entry for those considering Infinite Banking. One could argue that the cost does buy something–insurance. However, it is still a cost that must be taken into account.

Pro: Liquid and Accessible Capital

The next benefit is liquidity and access to capital.

With bonds, CDs, stocks, and mutual funds, you must sell the asset to access the capital.

That means you will take a hit to your capital if you need the money, but the asset is in flux.

If you are down, you must sell at a loss.

If you are up, you must pay taxes.

Either way, simply accessing your own money becomes a losing situation.

Whole life insurance offers liquidity and easy access to capital not found in most investment options.

With whole life, this is typically done by getting a loan through the life insurance company against the cash value in the policy.

It’s a quick and easy process that gives the individual access to the money they need for whatever they want, whenever they want.

Whether a smart investment opportunity arises or there are personal needs for accessing the money, whole life insurance offers liquidity and access to capital.

Con: Lack of Flexibility

Another downside of Infinite Banking is the lack of flexibility, especially when growing the policy.

An Infinite Banking policy is set up in reverse to a standard whole life policy.

Typically, when buying insurance, you start with the amount of insurance you want and then find out the premium, or payment, necessary to buy that insurance.

Infinite Banking is the opposite. To maximize the policy, Infinite Banking asks, “How much premium do I want to pay,” and then determines the least amount of life insurance possible.

This is done to maximize the cash value of the policy.

But because a policy is optimized for a specific premium, it will only be effective if that premium payment target is hit.

For instance, if you set up a policy at a $100,000 premium per year, but can only afford to put in $50,000 next year, this makes the policy less efficient.

And over time, the problem compounds.

Yes, there are ways to address these issues. However, this lack of simple flexibility makes Infinite Banking require more planning–making it inconvenient compared to other savings vehicles.

Pro: Tax-Advantaged

Next, we have the tax advantages of Infinite Banking.

There are three ways that Infinite Banking can offer tax advantages. They are:

- Dividends

- Loan Repayments

- Death Benefit

Dividends

The first is dividends.

Dividend payments are tax-free.

By keeping these dividends in the policy and not liquidating them, you can avoid taxes indefinitely.

If you consider the implications of taxes, the difference is significant.

Take the 8.61% growth of a life insurance policy over 30 years.

$100,000 growing over that time would increase to $1,191,501.

The account would grow to only $577,609 if this were taxed annually.

That’s almost a 50% total difference.

Taxes have a significant impact on future growth. Not only do taxes take away from the growth you have earned, but they also take away from the potential compounded growth of those taxed dollars.

Whole life insurance growth is not taxed. This tax saving makes a big difference to your potential wealth.

Loan Repayments

There are also tax savings for loan repayments. Any interest paid on that loan is tax deductible when taking a loan for business or investment purposes.

For Infinite Banking, when you take a loan, the life insuance company charges you around the same percentage you earn in the policy as dividends.

This means you get to write off the interest paid to your policy.

Another pro of Infinite Banking and whole life insurance.

Death Benefit

Lastly, there is the benefit of life insurance.

When you die, life insurance typically transfers to beneficiaries tax-free.

With Infinite Banking, this is what you rely on.

During your life, you let dividends build up. If you need access to capital, you simply take a loan from the life insurance company.

Then, when you die, the net death benefit–death benefit minus outstanding loans–transfers tax-free.

You avoid taxes on dividends while you are alive, and your beneficiaries get insurance death benefit transferred tax-free when you die.

This one-two punch makes whole life insurance effective as a tax-reduction strategy.

Con: Requires an Expert

The last negative of Infinite Banking is that it requires an expert.

Unlike a bank account or bond, you need help correctly setting up an Infinite Banking Concept policy.

The agent helping you has a lot of power. This is why you need someone you can trust.

A good agent will be beneficial and make the process easy.

Your policy may not be as effective if created by an inexperienced agent.

This means that the Infinite Banking agent you use makes a difference. And you need an expert to implement an Infinite Banking policy.

Conclusion

There is no one-size-fits-all investment approach. There are pros and cons of Infinite Banking. However, the benefits of Infinite Banking are worth exploring. It is a unique investment approach compared to traditional methods.

Whether you want to grow wealth, preserve capital, or save on taxes–Wise Money Tools can help. Our strategies are time-tested and proven. Contact us today for more information on how our services can help you reach our financial goals.